BP (BP)·Q4 2025 Earnings Summary

BP Beats on All Metrics, Suspends Buyback to Prioritize Balance Sheet

February 10, 2026 · by Fintool AI Agent

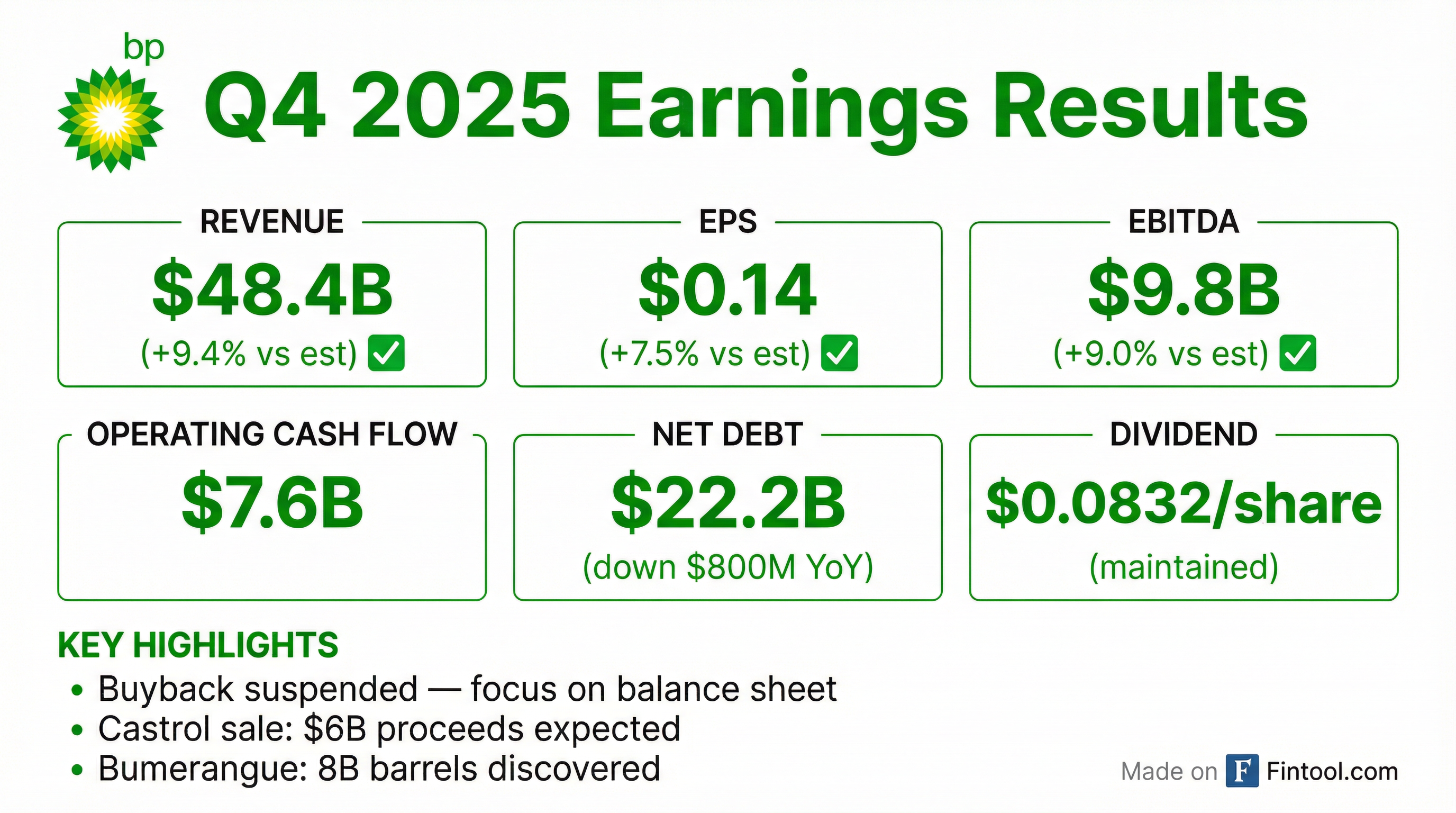

BP delivered a solid beat across revenue, EPS, and EBITDA in Q4 2025, but the headline story is a strategic pivot: the board has suspended share buybacks indefinitely to accelerate balance sheet repair. Combined with the Castrol divestment ($6B in proceeds) and a massive discovery in Brazil (8 billion barrels), BP is repositioning for the next cycle — at the expense of near-term shareholder returns.

Leadership Transition: Interim CEO Carol Howle (former head of trading) presented the results ahead of Meg O'Neill's arrival as CEO on April 1, 2026. Howle thanked outgoing CEO Murray for "34 years of service" while emphasizing the leadership team's conviction in BP's potential.

Did BP Beat Earnings?

BP beat consensus estimates across all three headline metrics:

Values retrieved from S&P Global

Full-year 2025 underlying replacement cost profit was $7.5 billion, with operating cash flow of $24.5 billion (including $2.9B working capital build). Capital expenditure fell 10% YoY to $13.6 billion organic.

Q4 operating cash flow was $7.6 billion, including $900 million working capital release. Net debt ended the quarter at $22.2 billion — down $800 million from year-end 2024.

What Did the Board Decide on Capital Allocation?

The major news: BP suspended its share buyback program. The 30-40% shareholder distribution guidance has been retired.

What changed:

Management framed this as creating "a stronger and more resilient platform to invest with discipline into our distinctive deep hopper of oil and gas opportunities."

What Were the Segment Results?

Q4 results by segment showed broad weakness vs. Q3, driven by lower commodity prices and seasonal factors:

Trading contribution: Supply, trading, and shipping delivered ~4% uplift to BP's returns for the sixth consecutive year — a "distinctive competitive advantage."

How Did the Stock React?

BP shares closed at $39.22 on the day of earnings — near 52-week highs ($39.51). The stock has rallied 55% from its 52-week low of $25.22.

Values retrieved from market data as of February 9, 2026

Despite the buyback suspension, the stock held near highs — likely supported by the beat, the Castrol proceeds, and the Bumerangue discovery.

What Changed From Last Quarter?

Positive shifts:

- ROCE improved to ~14% in 2025 (price-adjusted) vs. ~12% in 2024

- Reserves replacement ratio hit 90%, up from ~50% average in prior 2 years

- Divestments exceeding plan: $5.3B received in 2025 (above initial guidance)

- Structural cost reductions at $2.8B of $5.5-6.5B target

- Operational records: Plant reliability >96%, wells reliability ~98%, methane intensity 0.04% (well below 0.2% target)

- Major projects: 7 started in 2025 (5 ahead of schedule), IPA benchmarking "best in class" for start-up and stay-up

Negative shifts:

- Buyback suspended — CFO: "Reaching $14-18B net debt is not an automatic trigger to reinstate"

- $4 billion impairments on transition businesses (biogas, renewables) — "a deliberate decision to manage our pace of growth"

- Q4 IFRS loss of $3.4B due to impairments and inventory losses

- Net debt still elevated at $22.2B vs. $14-18B target

- Four fatalities in U.S. retail (roadside assistance) — BP permanently stopped roadside assistance next to active traffic lanes

What Did Management Guide for 2026?

Full-year 2026 guidance:

2027 Targets (confirmed):

- Net debt: $14-18B

- ROCE (price-adjusted): >16%

- Cost reductions: $5.5-6.5B (from $4-5B, incl. Castrol)

- Underlying OpEx: ~$19-20B

The underlying production guidance is "higher than expectation we gave this time last year," a positive signal on operational momentum.

What Are the Key Strategic Developments?

Bumerangue Discovery

BP announced its largest discovery in 25 years — 8 billion barrels of liquids in place (see detailed section below).

Castrol Divestment

BP agreed to sell 65% of Castrol for $6 billion in net proceeds at 8.6x EV/EBITDA — "at least as good as, if not better, than other precedent transactions." BP retains 35% to participate in future upside.

Transition Business Impairments

BP took $4 billion in after-tax impairments on its transition businesses, including biogas (Archaea) and renewables. Management acknowledged past overreach: "We went too far, too fast a number of years ago."

Lightsource bp Sale Process

BP has "interested parties who are looking very hard at Lightsource bp" and is "working through that" process.

Wood Mackenzie Ranking

BP now has the second longest remaining resource life among the majors, according to Wood Mackenzie benchmarking — 23 years at current production levels.

What Did Analysts Ask in the Q&A?

The Q&A session revealed important color on management thinking:

On Buyback Reinstatement (UBS, Goldman Sachs, Bank of America): CFO Kate Thomson was repeatedly pressed on when buybacks would resume. Her response: "Reaching the $14-18B net debt target is not an automatic trigger for us to reinstate the buyback. We need to take a holistic view of the balance sheet." She deferred major decisions to incoming CEO Meg O'Neill, who joins in April 2026.

On Capital Discipline (Barclays): When asked "What's different this time?", Interim CEO Carol Howle emphasized a "real cultural shift in cost and discipline" and that "every dollar has to compete within the portfolio." CFO Thomson acknowledged past missteps: "We went too far, too fast a number of years ago."

On Total Financial Obligations (Goldman Sachs): Thomson disclosed that BP's total financial obligations add up to ~$58 billion, including net debt, $12B in hybrid bonds, leases, and Gulf of Mexico settlement liabilities ($1.6B due in 2026, $1.2B in 2027).

On the Investment Case (BNP): Asked to articulate why investors should stay with BP despite suspended buybacks, EVP Gordon Birrell laid out a three-tier growth case:

- Short-term: Efficient base management (decline within 3-5%), 70% of wells in top two quartiles

- Medium-term: BPX growing to 650kboe/d with 45% IRR at $65 WTI; Paleogene online 2029-30

- Long-term: Bumerangue (early 2030s), Azule fields in Namibia, more Paleogene (10B barrels in place, only 600M in first projects)

On BPX (Wolfe, UBS): Management defended BPX as "a core part of BP" with exceptional economics: 7 billion barrels in place, #1-3 NPV per acre in all three basins (Permian, Eagle Ford, Haynesville), 20% improvement in completion time, and can now deliver the same annual resources with 8 rigs that previously required 10.

On AI and Technology (Barclays): Birrell highlighted two AI applications:

- Wells Advisor: AI system giving rig personnel instant access to 100+ years of drilling knowledge

- Kick Detection: AI-powered monitoring achieves 90% success rate detecting small kicks within roughly a minute, preventing potential blowouts

What Did Management Reveal About Bumerangue?

EVP Gordon Birrell provided new technical details on BP's largest discovery in 25 years:

Timeline:

- Appraisal program to start ~year-end 2026 using Transocean's Deepwater Mykonos rig

- Will drill Tupinambá exploration prospect first in neighboring block

- Early production system being considered

On Partnership: Birrell stated BP is "in no rush to take a partner" and would only do so "for value" with a partner who "can bring something to the table." BP currently holds 100% working interest.

Recoverable estimates: When pressed by Wolfe Research for recovery factors, Birrell declined: "I'd like to understand a bit more across the reservoir, what the variability is across the reservoir, before we put any more numbers."

What Management Avoided

Management did not provide:

- A timeline for resuming buybacks ("Ask me again in six months" — CFO Thomson)

- Specific net debt targets beyond the existing $14-18B range

- Detailed breakdown of the Bumerangue economics or timeline to first oil

- Clarity on what level of net debt would trigger buyback resumption

- Recoverable resource estimates for Bumerangue (only in-place volumes disclosed)

Forward Catalysts

Key Takeaways

- Triple beat — Revenue (+9.4%), EPS (+7.5%), EBITDA (+9.0%) all exceeded consensus

- Buyback suspended — Shareholder returns deprioritized; 30-40% OCF guidance retired

- Balance sheet first — Castrol sale ($6B), divestments, and impairments signal deleveraging priority; total financial obligations ~$58B

- Bumerangue upside — 8B barrel discovery (50/50 oil/condensate, 1,000m column) is BP's largest in 25 years; appraisal starting year-end 2026

- Transition pullback — $4B impairments on renewables/biogas; focus returning to oil & gas

- BPX strength — 45% IRR at $65 WTI, 7B barrels in place, capital productivity improving 20%+

- Leadership change — Meg O'Neill joins as CEO April 1; capital allocation decisions deferred to her arrival

This analysis was generated by Fintool AI Agent based on BP's Q4 2025 earnings transcript and financial data from S&P Global.

Related: BP Company Page | Q4 2025 Transcript | Q3 2025 Earnings